ITEMS PRESENTED AND DISCUSSED AT THE SEPTEMBER MEETING

Impact of Rising Inflation and Interest Rates on Financial Reporting

After a sustained period of low interest rates, interest rates are now rising in Canada. At its September 2022 meeting, the Bank of Canada raised its benchmark interest rate by 75 basis points to 3.25 per cent.1 This is the fifth consecutive increase since March 2022 as the Bank of Canada continues to tighten its monetary policy to help rein in inflation. A combination of rising inflation and an expectation of future interest rate hikes by the Bank of Canada also has resulted in an increase in Government of Canada bond yields.

Rising inflation and interest rates can have a wide impact on financial reporting. For example, they may impact the measurement of assets, liabilities, and net interest expense and trigger impairment losses. In addition, rising bond yields impact the pricing of long-term debt and equity instruments and enterprise value as the yields affect the cost of debt, the cost of equity and the weighted-average cost of capital (WACC).

The Group discussed various financial reporting considerations regarding rising inflation and interest rates. The issues the Group discussed are not exhaustive. Entities should consider their own circumstances when analyzing the impacts of rising inflation and interest rates on their financial statements.

Non-financial assets and leases

Impairment (IAS 36 Impairment of Assets)

Impairment tests for goodwill, intangible assets, items of property, plant and equipment, and right-of-use assets require companies to determine the recoverable amount of the individual asset, or the cash-generating unit (CGU) to which the asset belongs. The recoverable amount is the higher of the asset’s or CGU’s fair value less costs of disposal (FVLCD) and value in use (VIU). VIU represents the discounted net future cash flows associated with the continued use and ultimate disposal of the asset or the CGU. Impairment losses arise when the carrying amount of the asset or the CGU exceeds its recoverable amount.

The discount rate is a key input to calculate VIU and also FVLCD when an income approach is used. As discount rates are commonly estimated using the WACC formula, rising long-term risk-free interest rates may result in higher discount rates. Absent any offsetting adjustments to cash flow projections, higher discount rates may reduce the VIU or FVLCD of an asset or CGU. This can indicate an asset may be impaired, even if previous impairment tests showed significant headroom.

Estimates of future cash flows and the discount rate reflect consistent assumptions about price increases attributable to general inflation. Therefore, if the discount rate includes the effect of price increases attributable to general inflation, future cash flows should also include general inflation expectations and vice versa.

Lease assets and lease liabilities (IFRS 16 Leases)

A lessee reports the lease liabilities and right-of-use assets at amounts that reflect discounted lease payments. Discount rates are often based on a lessee’s incremental borrowing rate.

Although the discount rate is typically not revised throughout the lease term, some events that trigger a remeasurement of existing lease liabilities would require the lessee to revise the discount rate to reflect conditions at the date of remeasurement. Examples of these events include changes in lease payments due to a change in floating interest rates, changes in the lease term, and certain lease modifications. For those entities that need to remeasure existing lease liabilities at a revised discount rate, rising interest rates can drive higher discount rates, lower lease liabilities, and lower corresponding right-of-use assets. Consequently, in the long run, a greater proportion of the lease expenses recognized could shift from amortization to interest expense.

The Group’s Discussion

Group members agreed with the analysis.

Several Group members observed that rising interest rates have reduced the headroom from previous impairment tests and triggered impairment testing. As rate hikes are expected to continue in Canada, these Group members noted entities should closely monitor their impact on the valuation models. Given the reduced headroom, some Group members noted that entities may need to perform a detailed impairment test during interim financial reporting periods, rather than rely on the detailed calculations used in the most recent annual impairment test.

Group members then discussed the impact of the current economic environment on the components of the valuation model. A few Group members noted that the growth rate used to calculate the terminal value incorporates long-term economic forecasts. They observed that the long-term growth rate is still targeted at a rate much lower than the current inflation rate. Consequently, the growth rate may not offset the impact of higher discount rates used in the recoverable amount calculation. Some Group members also noted that rising rates could also impact broader cash flow projections, including pricing and costing structures. In addition to interest and inflation rates, they observed that factors such as customer demand and geopolitical issues may impact the cash flow projections in the valuation model. They noted that these factors should be considered holistically in the valuation model to determine the recoverable amount of an asset or a CGU.

The Group also considered the disclosure implications around management estimates and judgments made in the impairment analysis. Given that discount rates are often a critical management estimate, some Group members commented that entities should consider requirements in IAS 1 Presentation of Financial Statements on significant judgments and sources of estimation uncertainty. In addition, these Group members noted that entities should consider whether their annual IAS 36 disclosures may require an update in their interim financial statements. In particular, updated disclosure may be warranted of any sensitivity analysis around a reasonable possible change in a key assumption in paragraph 134(f) of IAS 36.

Financial instruments (IFRS 9 Financial Instruments)

Measurement

After initial recognition, financial assets, and financial liabilities are measured at amortized cost or fair value. For floating-rate financial instruments measured at amortized cost, their accounting may be affected by rising interest rates as anticipated cash flows may need to be re-estimated to reflect current and expected conditions. Any period re-estimation of cash flows will affect the effective interest rate of a floating-rate financial asset or financial liability.

Rising interest rates will directly affect the measurement of financial assets or financial liabilities measured at fair value since their value is commonly based on discounted cash flows.

Expected credit losses (ECLs)

The ECL model covers, among other items, financial assets measured at amortized cost and investments in debt instruments measured at fair value through other comprehensive income. ECLs are based on the present value of expected cash shortfalls. The rate to discount ECLs is the original effective interest rate, unless the financial asset has a floating rate, in which case the current effective interest rate is used. Therefore, ECLs for floating-rate financial assets may be lower due to the effect of higher discount rates. However, any such reduction in ECLs could be offset by potential increases in the estimates of cash shortfalls if borrowers are adversely affected by rising interest cost and inflation.

Derivatives and hedge accounting

Rising interest rates may affect the fair value measurement of derivatives, along with the hedge effectiveness assessment of any related hedging relationships. In addition, entities may also seek to close out existing hedge positions and terminate hedging relationships.

On the other hand, rising interest rates may also motivate entities to enter into derivatives or other hedging arrangements to limit the exposure to interest rate risk.

The Group’s Discussion

Group members agreed with the analysis.

Some Group members observed that in financial institutions, the inflation outlook and the possibility and the severity of a recession are considered as forward-looking information and are incorporated in the ECL calculation. As a result, some financial institutions may have increased their ECL reserves to reflect these macro-economic uncertainties. They also noted that because of the timing differences between re-pricing of financial assets and financial liabilities, some financial institutions may encounter pressure on their net interest margin.

For corporate entities, a few Group members noted that rising interest rates and inflation can increase the cost of borrowing and reduce liquidity for their customers. They also observed that the credit spread for many entities widened in 2022. Therefore, entities should monitor their customers’ credit in the current economic environment and consider its impact on their ECL calculation.

Employee benefits and provisions

Defined benefit plans (IAS 19 Employee Benefits)

Rising interest rates can have a significant impact for entities with defined benefit pension plans as higher discount rates may affect various areas of measurement, including:

- present value of the defined benefit obligation;

- fair value of plan assets;

- asset ceilings on plan surpluses (present value of certain economic benefits);

- net interest on the net defined liability (asset), recognized in the income statement; and

- remeasurement gains or losses recognized in other comprehensive income or loss.

While rising interest rates reduce defined benefit obligations, inflation and rising costs may have an offsetting impact on the underlying valuations. Entities may also need to consider whether any changes to future funding levels may be required.

Canadian entities that sponsor defined benefit plans are required to monitor for significant market fluctuations during the interim financial reporting period. Some key drivers that may result in significant market fluctuations include economic assumptions, specifically the discount rate and inflation, and the market value of both financial and non-financial assets at the measurement date.

Some defined benefit pension plans may have limits imposed on the net asset or liability positions in accordance with IFRIC Interpretation 14 IAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction. These entities should consider whether they need to remeasure the net defined benefit liability or asset during interim financial reporting periods.

Determining whether there is a need to remeasure the net defined benefit liability or asset for interim financial reporting requires judgment. The potential materiality of a remeasurement is assessed in relation to the interim financial statements.

Provisions (IAS 37 Provisions, Contingent Liabilities and Contingent Assets)

Where the effect of the time value of money is material, a provision shall be measured at a discounted amount, being the present value of the expenditures expected to be required to settle the obligation. Rising interest rates could lead to more long-term provisions needing to be discounted. Examples of long-term provisions that may be impacted include decommissioning or asset retirement obligations, especially in the extractive industry. In addition, the impact of higher discount rates on the provision may be offset by rising costs and risk adjustments. Finance expenses may increase because the unwinding of the discount is presented as interest costs.

Rising inflation may also trigger inflation adjustments. While IAS 37 provides no guidance on whether the discount rate should include the effects of inflation, in practice, companies ensure they use a consistent approach: If the cash flows are expressed in current prices, the effects of inflation are not included in the discount date (i.e., a real discount rate is used). If the cash flows include inflation, the discount rate also includes the effects of inflation (i.e., a nominal discount rate is used).

The Group’s Discussion

Group members agreed with the analysis.

Regarding the impact on defined benefit plans, one Group member noted that rising inflation and interest rates may also impact other actuarial assumptions. Therefore, entities should consult with their actuaries to update key assumptions (e.g. demographic data and wage inflation) to ensure these actuarial assumptions are consistent.

One Group member commented that the decommissioning obligation related to a property, plant, or equipment may increase when the effects of inflation are greater than the effects of the rising discount rate. Consequently, the higher decommissioning obligation reduces the carrying value of the asset base. This Group member commented that the carrying value of the asset should be reduced prior to the CGU being tested for impairment. Another Group member also highlighted the disclosure requirement in paragraph 84 of IAS 37 which requires the entity to disclose the effect of any change in the discount rate on its provisions.

One Group member noted that entities with fixed price contracts should consider the impact of rising costs and assess whether they have become onerous based on the guidance in IAS 37.

Other matters

Revenue recognition (IFRS 15 Revenue from Contracts with Customers)

The effect of the prevailing interest rates in the relevant market is one factor an entity should consider when assessing whether a contract contains a financing component and whether that financing component is significant. As a result, rising interest rates may affect the entity’s assessment of whether a new contract with a customer contains a significant financing component. Entities that provide financing to their customers may see a reduction in revenue and an increase in interest income.

Borrowing costs (IAS 23 Borrowing Costs)

Borrowing costs are capitalized if they are directly attributable to the acquisition, construction, or production of qualifying assets. Qualifying assets are generally assets that are subject to major development or construction projects. Borrowing costs eligible for capitalization will likely increase with rising interest rates because interest expense would be expected to increase.

Financial statement disclosures

There are differences in the specific disclosure requirements for present value measurements between IFRS 13 Fair Value Measurement, IAS 19, IAS 36 and IAS 372. For example, disclosure of the discount rate itself is not required by all standards, and the method used to determine discount rates is not always required to be disclosed. Due to these differences in the disclosure requirements, entities need to apply judgment to determine what information should be disclosed.

For financial instruments, entities should disclose the nature and extent of the risks arising from them and the related mitigation efforts. These disclosures generally include both qualitative and quantitative information.

Entities should also consider disclosure requirements pertaining to the sources of estimation uncertainty in IAS 1 and any changes in accounting estimates under IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors. They also need to exercise judgment when considering the disclosure requirements in IAS 34 Interim Financial Reporting when preparing interim financial statements.

The Group’s Discussion

The Group agreed with the analysis.

Several Group members commented that given the recent changes in the macroeconomic environment, entities should consider the disclosure requirements in various IFRS Accounting Standards and make necessary updates to disclosures from previous reporting periods. For example, entities should examine whether the sensitivity analysis around the range of reasonable expectations needs to be broadened considering the changes in interest rates, inflation, commodity prices, and other economic factors. Entities should also reflect the changes in the economic environment in their disclosures around risks such as interest rate risk, liquidity risk, and counterparty credit risk.

Several Group members observed that rising interest rates may also have broader implications on other assets that are measured at fair value, such as investment properties and biological assets. The rising discount rates may reduce the fair value of these assets and the net income of those entities in, for example, real estate investment and cannabis industries. If these reductions are significant, entities may risk violating their debt covenants that are based on net income or earnings before interest, taxes, depreciation and amortization, which may result the debt being classified as current liabilities on their balance sheet. An observer highlighted that entities need to closely monitor and incorporate the impact of rising rates in their forecasts to identify any issues with loan covenants to allow them to work with their lenders on obtaining any necessary relief on their loans before the reporting date.

Some Group members considered the additional pressure some entities may face when refinancing their loans at higher interest rates. The additional interest costs combined with the overall rising costs of doing business may cast significant doubt about their ability to continue as a going concern. These Group members noted entities should update their going-concern assessment to incorporate rising inflation and interest rates and other relevant economic factors to support their ability to continue as a going-concern. A representative of the Canadian Securities Administrators emphasized that the entities in so-called close-call situations should disclose key assumptions and judgments made in concluding that there are no material uncertainties related to events or conditions that may cast significant doubt upon their ability to continue as a going concern.

In addition to financial reporting topics discussed in the analysis, a few Group members raised the impact of rising inflation and interest rates on the following topics:

- IFRS 17 Insurance Contracts – the measurement of insurance contract liabilities;

- IAS 12 Income Taxes – the ability to realize any deferred tax assets;

- IFRS 14 Regulatory Deferral Accounts – accounting for rate regulated deferral account balances;

- IAS 1 Presentation of Financial Statements – disclosing information, if material, about the impact of rising rates on the recognition and measurement of financial statement items; and

- IAS 10 Events after the Reporting Period – assessing whether subsequent events are adjusting or non-adjusting events and the need to provide additional disclosure on interest and inflation rate increases after the reporting date.

Overall, the Group’s discussion was to raise awareness of the pervasive impact of the rising interest rates and inflation environment on many standards. The Group emphasized that entities should stand back and carefully contemplate all the implications of the current environment on the financial statements. No further actions were recommended to the AcSB.

1 Bank of Canada, “Bank of Canada increases policy interest rate by 75 basis points, continues quantitative tightening,” press release, September 7, 2022.

2 IASB, “Project Summary, Discount rates in IFRS Standards,” appendix A, February 2019, 15.

Back to top

Financial Reporting Implication of OECD Pillar Two GloBE Rules

In October 2021, 137 of 140 countries in the Organisation for Economic Co-operation and Development (OECD)/G20 Inclusive Framework on Base Erosion and Profit Shifting (“Inclusive Framework”) reached a landmark agreement to implement a two-pillar solution to reform the international taxation rules in response to challenges relating to the taxation of the digital economy. The two-pillar solution introduces a new global corporate minimum tax.

In December 2021, the OECD released the Pillar Two model rules (also known as the Global Anti-Base Erosion Rules (GloBE Rules)), which provide pivotal information on how the minimum tax works. While each jurisdiction needs to decide whether to adopt the GloBE Rules and when, the OECD has announced the GloBE Rules should be enacted by the various jurisdictions into domestic legislation in 2022, to be effective in 2023.

The Group discussed the following questions:

- What are the GloBE Rules, at a high level?

- What are the potential financial reporting implications of the GloBE Rules?

- What action might management want to take now?

Issue 1: What are the GloBE Rules, at a high level?

Analysis

The GloBE Rules are proposed international tax rules designed to ensure that large multi-national enterprises (MNEs) within the scope of the Rules pay a minimum level of tax of 15 per cent on the income arising in each jurisdiction in which they operate. If a MNE has an effective tax rate that is less than 15 per cent in a jurisdiction, it will have to pay a top-up tax for the difference. In general, it is expected that the top-up tax will be paid by the MNE’s ultimate parent entity, with the tax being due to the parent entity’s local tax authority.

The goal of the GloBE Rules is to end the ‘race to the bottom’ where certain countries have been reducing their corporate tax rates to attract foreign investment which has led to other countries feeling compelled to reduce their corporate tax rates to remain competitive.

The GloBE Rules apply to MNE groups if the revenue in their consolidated financial statements exceeds EUR 750 million, in two of the last four fiscal years. The GloBE Rules do not apply to government entities, international organizations and non-profit organizations nor do they apply to entities that meet the definition of a pension, investment or real estate fund. These entities are excluded even if the MNE group they control remains subject to the rules.

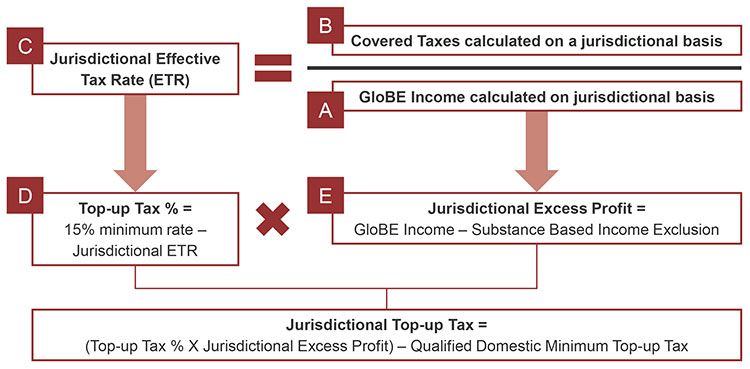

The following diagram outlines at a high-level the process for calculating the jurisdictional top-up tax. The components of the diagram are described in the paragraphs that follow. This report does not address all of the detailed steps and requirements in the GloBE Rules for determining the top-up tax which are detailed, nuanced and based on specific defined terms in the GloBE Rules.

To know if they owe top-up tax, MNEs need to calculate the jurisdictional effective tax rate (ETR) for each jurisdiction in which the MNE group operates. This requires a calculation of the GloBE income or loss, and the covered taxes on such income for each constituent entity in the group.

[A] The GloBE income or loss: A constituent entity starts by taking its financial accounting net income or loss for the fiscal year that is used for preparing consolidated financial statements of the ultimate parent entity prior to elimination of intragroup items. Adjustments are then made to eliminate common book-to-tax differences including those relating to dividends, equity method income, stock-based compensation, accrued pension expense, revaluation gains and losses, and certain foreign currency gains and losses.

[B] The covered taxes: A constituent entity starts with its current tax expense for the fiscal year that is used in preparing the consolidated financial statements of the ultimate parent entity. Adjustments are made to current tax expense for various items including uncertain taxes and refundable tax credits. Adjustments are also made to consider temporary differences using an entity’s deferred tax expense (income) as a starting point to which various adjustments are made for GloBE purposes. For instance, there is an adjustment to recast deferred tax expense using a tax rate of 15 per cent, where a tax rate higher than 15 per cent was used. This is a unique use of deferred taxes in a tax calculation.

[C] The jurisdictional ETR: An MNE Group is required to determine the ETR for each jurisdiction in which it operates which is the amount of covered taxes with respect to a jurisdiction divided by the GloBE Income for such jurisdiction. When the ETR for the jurisdiction is less than the minimum rate of 15 per cent, then the top-up tax percentage must be calculated.

[D] The top-up tax percentage: This is the minimum rate of 15 per cent less the ETR for the jurisdiction (e.g., if the ETR is 10 per cent, the top-up tax percentage is 15%-10%=5%). The jurisdictional top-up tax is calculated by applying the top-up tax percentage to the excess profit for the jurisdiction (i.e., the GloBE Income for the jurisdiction less a substance based income exclusion).

[E] The substance based income exclusion: This is a reduction to the profit subject to the minimum tax for substantive activities in the jurisdiction. It is calculated as a percentage of payroll costs incurred and tangible assets located in the jurisdiction. Finally, the top-up tax is reduced by any applicable qualified domestic minimum top-up tax.

Once the amount of the top-up tax is calculated it is necessary to determine which entity(ies) in the MNE group is liable to pay such tax. Under the income inclusion rule (IIR), the minimum tax is paid at the level of a parent entity, in proportion to its ownership interests in those entities in low-taxed jurisdictions. Generally, the IIR is applied at the level of the ultimate parent entity and works its way down the ownership chain. If there is any residual top-up tax that remains unallocated after the IIR is applied, the under taxed payment rule (UTPR) applies to allocate the tax to other members of the group (e.g., a sister subsidiary in respect of a low-taxed subsidiary).

The GloBE Rules contemplate the possibility that countries may introduce their own domestic minimum top-up tax regime. If countries implement a domestic minimum top-up tax regime that fully complies with the GloBE Rules and increases the domestic tax liability for entities within the jurisdiction to at least 15 per cent, no incremental top-up tax would be due under the GloBE Rules. However, if such domestic tax regimes do not fully comply with the GloBE Rules, additional top-up taxes under GloBE may still be due.

Implementation and timing

The GloBE Rules are intended to be implemented as part of a ‘common approach’, as agreed by the OECD members. This means that jurisdictions are not required to adopt the GloBE Rules, but if they choose to do so, they will adopt them consistently with the model.

Given that the OECD does not have the power to implement tax legislation in any country, each country will need to determine if and when the GloBE Rules will be enacted. The OECD has announced the rules should be brought into domestic legislation in 2022, to be effective in 2023 with the UTPR coming into effect in 20243. Canada proposes to implement the Pillar Two Rules, along with a domestic minimum top-up tax and IIR that would be effective in 2023, and the UTPR effective not before 2024.4

The following are some initial observations on implementation:

- The GloBE Rules are detailed and complex and it will likely take time to assess their impact.

- It will be necessary to determine how the GloBE Rules interact with any domestic minimum top-up tax regimes to be enacted, and existing regimes such as the US Global Intangible Low Taxed Income (GILTI) regime.

- If some countries choose to adopt the GloBE Rules, but others choose not to adopt at all, or choose not to adopt them at the same time, this could create additional complexity.

- Entities will need to obtain a refreshed understanding of their tax and legal structures around the world.

- The finance and tax departments would need to work closely in assessing the impacts of the GloBE Rules – which includes identifying entities operating in jurisdictions which are potentially taxed below the 15 per cent minimum rate.

The Group’s Discussion

Group members agreed with the analysis, noting that the GloBE Rules are detailed and complex and will require significant effort to implement.

One Group member observed that some multi-national organizations in Canada expect the rules will be substantively enacted in Canada and have already initiated the process to assess the impact of the rules on their operations.

Some Group members noted that given the calculation of GloBE income and loss starts with the financial accounting income or loss used in preparing the ultimate parent entity’s consolidated financial statements, it is based on the accounting standard used in the ultimate parent’s consolidated financial statements (e.g. IFRS Accounting Standards). The standard used in such consolidated financial statements may be different from that used in a subsidiary’s statutory financial statements, unless an exception is met. As a result, some entities may need to maintain another set of financial records for GloBE purposes, in addition to their existing records for financial accounting and tax reporting under the rules in their local jurisdictions. These Group members noted such effort can be significant to MNEs.

Issue 2: What are the potential financial reporting implications of the GloBE Rules?

The proposed GloBE Rules raise several accounting questions, such as whether the top-up tax is an income tax in the scope of IAS 12 Income Taxes, and if so, when and how entities should account for the new taxes. As the GloBE Rules are not yet effective, discussion of the potential accounting implications is still underway. The following are key questions an entity might consider when adopting the GloBE Rules.

Question 1: Are the top-up taxes imposed by the GloBE Rules in scope of IAS 12?

Analysis

IAS 12 applies to taxes that are based on taxable profits. At the highest level, the top-up taxes are based on financial accounting income or loss, with various adjustments. Therefore, one might view the top-up taxes as income taxes in the ultimate parent entity’s consolidated financial statements.

However, as the OECD noted, the top-up taxes imposed by the GloBE Rules do not operate as a typical direct tax on income of an entity. They apply to excess profits calculated on a jurisdictional basis and only apply to the extent those profits are subject to tax in a given year below the minimum rate. As a result, rather than a typical direct tax on income, the tax imposed under the GloBE Rules is closer in design to an international alternative minimum tax. This raises the question on whether these taxes are in the scope of IAS 12, in particular the UTPR which may result in top-up taxes being allocated among various entities in the group including those outside of the jurisdiction. Therefore, a detailed assessment of these taxes and an understanding of how these rules are enacted in each jurisdiction is necessary before concluding whether and how IAS 12 may apply to the group financial statements and separate entity financial statements.

Question 2: When are the changes in tax laws considered to be substantively enacted?

Analysis

IAS 12 requires that income tax assets and liabilities are measured using the tax rates (and tax laws) that have been enacted or “substantively enacted” by the end of the reporting period. While IAS 12 is not explicit as to when “substantive enactment” occurs, it is generally at the stage of the legislative process when the remaining steps will not change the outcome.

In Canada, a proposed change in income tax laws or income tax rates is generally not considered to be “substantively enacted” until detailed draft legislation has been tabled for first reading in Parliament. If there is a minority government, proposed amendments to the Income Tax Act would not normally be considered as “substantively enacted” until the proposals have passed third reading in the House of Commons.

MNEs will need to monitor the legislative developments with respect of substantive enactment of the GloBE Rules in all of the jurisdictions in which they operate either through wholly or partially-owned subsidiaries, joint ventures, flow-through entities or permanent establishments. Different countries may substantively enact the rules on different dates and with variations to the GloBE Rules, which will result in additional complexity in accounting for the GloBE Rules.

Question 3: Would the GloBE Rules affect the accounting for deferred taxes?

Analysis

Determining the deferred tax effects of the GloBE Rules can be complex. For example, there may be some expenses recognized in financial accounting net income or loss that are not deductible under the GloBE Rules and, therefore, are added back to arrive at GloBE income. However, those expenses may be deductible for GloBE purposes in future when paid. This raises a question on whether this gives rise to deferred taxes under IAS 12 (i.e., whether this is a temporary difference). If it does, entities should consider what tax rate should be used to measure the deferred tax. This determination can be complex as the top-up tax rate applicable to the reversal of GloBE income items will be contingent on future events, including:

- permanent differences related to local tax laws;

- aggregate future accounting income or loss of all entities in a particular jurisdiction; and

- other items that are difficult to forecast reliably.

Question 4: What should an entity consider disclosing in their interim and annual financial statements regarding the GloBE Rules?

Analysis

Paragraph 88 of IAS 12 requires that “where changes in tax rates or tax laws are enacted or announced after the reporting period, an entity discloses any significant effect of those changes on its current and deferred tax assets and liabilities (see IAS 10 Events after the Reporting Period).” (emphasis added)

Given the complexity of the GloBE Rules, it is expected that some entities will need time to assess how the rules affect their financial statements. This is complicated by the fact that, as noted in Question 3, it is not immediately apparent how to account for the top-up tax under IAS 12. Therefore, if local legislation is announced or enacted between the reporting period end and the date the financial statements are authorized for issue, an entity may not be able to fully determine the quantitative impact of the GloBE Rules on its current and deferred taxes. However, it would be reasonable that an entity should provide qualitative disclosure of the expected effects of the GloBE Rules on the entity’s business, and quantitative disclosure to the extent possible. Where entities are still in the process of assessing the effect of the rules, they should make a statement to that effect.

Even if the local legislation to implement the GloBE Rules is not announced or enacted before the financial statements are authorized for issue, an entity should consider providing qualitative disclosures of how the GloBE Rules could reasonably affect the entity in accordance with the requirement of paragraph 17(c) of IAS 1 Presentation of Financial Statements. This paragraph requires an entity to provide additional disclosures when compliance with the specific requirements in IFRS Accounting Standards is insufficient to enable users to understand the impact of particular transactions, other events and conditions on the entity’s financial position and financial performance. This disclosure requirement applies to both annual and interim financial statements. Such disclosure is also consistent with the fact that the GloBE Rules are unique in that the OECD has published model rules, which local tax authorities are expected to use when developing GloBE Rules-compliant legislation. As a result, investors may expect companies to assess the potential impacts of GloBE Rules before changes in local tax legislation are finalized.

Entities should exercise judgment when considering the nature and extent of disclosures, incorporating their circumstances and users’ expectations. These disclosures may include the following information about the group (some of which is based on quantitative information, which companies might consider providing, when it is reasonably determinable):

- Whether a material portion of its business operations is in relatively low-tax jurisdictions that are likely to be impacted;

- Those operations in low-tax jurisdictions with an ETR lower than 15 per cent;

- Those operations in jurisdictions where the government provides support through tax incentives, tax exemptions or additional deductions, resulting in an ETR lower than 15 per cent;

- Information about expected enactment of tax laws and their effective dates;

- Information about management’s assessment of the possible impacts, indicating they are not yet known or reasonably estimable.

The Group’s Discussion

Group members agreed with the analysis.

On Question 1, based on reading the current GloBE Rules, some Group members thought that at a high level, the top-up taxes are based on an entity’s financial accounting income or loss. Therefore, they thought that the top-up taxes imposed by the GloBE Rules are in the scope of IAS 12. However, they noted that when the rules are substantively enacted in each jurisdiction, an additional assessment of the GloBE Rules is needed to conclude whether IAS 12 applies. These Group members also observed that determining whether GloBE Rules create temporary differences that give rise to deferred taxes is complex. For jurisdictions that substantively enact the GloBE Rules before the end of 2022, entities should complete this analysis and reflect the accounting impact of the deferred taxes in their 2022 financial statements.

On Question 4, some Group members noted that investors find information related to events that can materially affect the entity’s future performance to be valuable. Therefore, entities should consider providing qualitative disclosure of the expected impacts of GloBE Rules on their business, and quantitative disclosure to the extent possible. They noted that the information should be consistent between financial statements and other corporate filings such as the management discussion and analysis.

One Group member also noted that entities should consider providing disclosures on non-adjusting events as required by paragraph 22 in IAS 10 regarding changes in tax rates or tax laws enacted or announced after the reporting period that have a significant effect on current and deferred tax assets and liabilities. Furthermore, this Group member observed that the cash payment related to the top-up tax could be significant and the resulting effect on liquidity may impact an entity’s going concern assessment. Entities should consider any potential payment related to the GloBE Rules in the expected cash flow when performing the going concern assessment.

Another Group member noted that given the complexity of the rules, entities should also consider the requirement in IFRIC 23 Uncertainty over Income Tax Treatments on how to apply the recognition and measurement requirement in IAS 12 when there is uncertainty over income tax treatments.

Issue 3: What actions might management want to take now?

Analysis

Considering the potentially significant impacts that the GloBE Rules can have on a MNE that is in scope of the rules, management should consider the following action plan to implement the GloBE Rules:

- Determine whether the MNE falls within the scope of the rules as currently set out by the OECD.

- Consider whether group companies operate in low-tax jurisdictions or jurisdictions where they benefit from tax incentives, tax exemptions or significant tax deductions that may result in a low ETR.

- Engage with tax specialists now to help assess the impacts of the GloBE Rules. This may include the following:

- Delineating between entities that will clearly exceed the minimum ETR threshold versus those that may not.

- Modelling the effective tax rates in the various jurisdictions.

- Estimating potential additional GloBE tax liabilities.

- Identify whether there are any challenges to obtaining data necessary to perform the calculations based on the model rules.

- Monitor the implementation of the GloBE Rules in relevant jurisdictions, particularly on when the rules are substantively enacted in their tax laws.

- Engage with users to determine the appropriate level of disclosures for both the 2022 interim and annual financial statements.

Pillar Two is new and the issues associated with its implementation and accounting are evolving. Management of in-scope MNEs should actively monitor developments in the jurisdictions in which they operate and develop an action plan appropriate to their particular circumstances.

The Group’s Discussion

Group members agreed with the analysis.

One Group member commented that given the complexity and operational challenges noted in the analysis, the entity may consider building an internal reporting process and management controls to ensure accurate and timely information is reflected in the consolidated financial statements.

Another Group member also noted that entities may need to engage with their auditors and tax professionals in the process of implementing the GloBE Rules.

Overall, the Group’s discussion raised awareness of the GloBE Rules and the associated financial reporting issues. An observer commented that the International Accounting Standards Board (IASB) is actively monitoring the development of GloBE Rules and considering whether urgent amendments to IFRS Accounting Standards might be needed concurrent with substantive enactment of tax legislation. Considering the GloBE Rules are expected to be substantively enacted in Canada as early as 2023 and the IASB’s activity in this area, the Group will monitor this issue for future developments. No further action was recommended to the AcSB.

3 OECD, “Statement on a Two-Pillar Solution to Address the Tax Challenges arising from the Digitalisation of the Economy”, October 8, 2021, 5.

4 Canada 2022 Budget, A Plan to Grow our Economy and Make Life More Affordable, Chapter 9, 210.

Back to top

IAS 12: Deferred Taxes Related to Assets and Liabilities Arising from a Single Transaction

The Group discussed the potential implications of the amendments to IAS 12 Income Taxes, for Deferred Taxes Related to Assets and Liabilities Arising from a Single Transaction, issued in May 2021. The amendments are effective for reporting periods beginning on or after January 1, 2023, with early application permitted.

Certain types of transactions are accounted for by recognizing both an asset and a liability. For example:

- under IFRS 16 Leases, a lessee recognizes both a right-of-use asset and a lease liability at the commencement date of a lease; and

- under IAS 16 Property, Plant and Equipment, an entity recognizes the initial estimate of a decommissioning obligation in both the cost of the asset and as a provision under IAS 37 Provisions, Contingent Liabilities and Contingent Assets.

The general principle in IAS 12 is for entities to recognize deferred tax assets for transactions that result in deductible temporary differences and deferred tax liabilities for transactions that result in taxable temporary differences. There is, however, an exemption to the requirement to recognize deferred taxes when, at the time of the transaction, the transaction affects neither accounting profit nor taxable profit (the “initial recognition exemption”).

Depending on the applicable tax law, some transactions may result in equal and offsetting temporary differences. Prior to the issuance of the amendment, there was diversity in practice in terms of applying the initial recognition exemption to such transactions.

As a result, the IASB issued an amendment to IAS 12 to exclude transactions that give rise to equal taxable and deductible temporary differences from the initial recognition exemption. In applying this amendment, entities will be required to recognize these equal and offsetting temporary differences in their financial statements.

The Group discussed the application of this amendment as it applies to a lessee recognizing both a right-of-use asset and a lease liability at the commencement date of a lease.

Issue 1: In Canada, do the tax deductions relate to the asset or liability?

Analysis

Entities should apply judgment to determine whether tax deductions relate to a leased asset (i.e., tax deductions for capital cost allowance) or a lease liability (i.e., tax deductions when an entity makes lease payments) by considering the applicable tax law.

In Canada, lease payments for assets used in an entity’s business are normally deducted in the year they are incurred. As a result, under Canadian tax law, tax deductions for a lease often relate to the lease liability.

However, the entity needs to apply judgment to determine this. For example, under certain conditions, and with the agreement of the lessor, a partnership (lessee) may choose to treat lease payments as combined payments of principal and interest. In those cases, the lessee would be considered (for tax purposes) to have purchased the asset by borrowing an amount equal to its fair market value, rather than having leased the asset. The lessee could then deduct the interest portion of the payment as an expense and could also claim capital cost allowance on the asset. The lessee might determine that the tax deductions relate to the leased asset in such a case.

The Group’s Discussion

The Group agreed with the analysis.

Some Group members pointed out that many Canadian entities have operations in other jurisdictions subject to different tax laws. These entities should review the wording in the applicable tax law in each jurisdiction where they operate and apply judgment to determine whether the tax deductions relate to the leased asset or the lease liability.

Issue 2: How does the allocation of tax deductions to either the asset or the liability affect the determination of temporary differences on initial recognition?

Analysis

Tax deductions related to the leased asset

When the tax deductions relate to the leased asset, the tax bases of the leased asset and lease liability are equal to the carrying amount of the leased asset and lease liability, respectively. As a result, no temporary differences arise on initial recognition of the lease and the initial recognition exemption does not apply.

The lessee would not recognize any deferred taxes on initial recognition because there are no temporary differences at that time. The lessee will subsequently recognize deferred taxes if temporary differences arise after initial recognition.

Tax deductions related to the lease liability

When the tax deductions relate to the lease liability, the tax bases of both the leased asset and lease liability are zero. As a result, a taxable temporary difference with respect to the leased asset and a deductible temporary difference with respect to the lease liability arise.

Under the amendments to IAS 12, the initial recognition exemption would not apply to the extent that the taxable and deductible temporary differences are equal. The lessee would therefore recognize both a deferred tax asset and deferred tax liability on initial recognition of the lease transaction.

The Group’s Discussion

The Group agreed with the analysis.

Some Group members pointed out that the purpose of the amendment is to eliminate diversity in practice. Therefore, some entities will not need to change practice if they already do not apply the initial recognition exemption to deferred taxes related to assets and liabilities arising from a single transaction. One Group member noted that entities that change practice as a result of this amendment should consider the additional disclosure requirements related to deferred taxes under IAS 12.

One Group member noted that entities might need to present the offsetting deferred tax asset and deferred tax liability as a net balance on their balance sheet. Paragraphs 74-75 of IAS 12 provide guidance on when deferred tax assets and liabilities should be offset for presentation purposes.

Another Group member noted that the outcome of applying the amendment is a consistent effective income tax rate, whether the lease payments relate to the leased asset or lease liability.

Some Group members commented that some lease agreements include advance lease payments and other initial direct costs. These Group members indicated that entities should account for the deferred tax impact of these payments.

Issue 3: If the entity does not recognize a deferred tax asset on initial recognition of the transaction because of the recoverability requirement in IAS 12, does this impact the recognition of any deferred tax liability?

Analysis

Paragraph 24 of IAS 12 only allows an entity to recognize deferred tax assets “to the extent that it is probable that taxable profit will be available against which the deductible temporary difference can be utilized” (i.e., the “recoverability requirement”). Therefore, this might result in an entity recognizing unequal deferred tax assets and liabilities even if the taxable and deductible temporary differences are equal.

An entity should continue to recognize a deferred tax liability for all of the taxable temporary differences that arise on initial recognition of the transaction. In accordance with paragraph 22(b) of IAS 12, any difference from the offsetting deferred tax asset should be recognized in profit or loss as a deferred tax expense. At the end of each reporting period, the lessee would need to reassess any unrecognized deferred tax assets that were not recognized as a result of the recoverability requirement.

The Group’s Discussion

The Group agreed with the analysis.

Issue 4: What are the next steps for transition?

Analysis

For most types of transactions, entities should apply the amendments to transactions that occur on or after the beginning of the earliest comparative period. For leases and decommissioning obligations, an entity must apply the amendments for the first time by recognizing deferred tax for all temporary differences at the beginning of the earliest comparative period presented. These transition requirements also apply to first-time adopters at the date of their transition to IFRS Accounting Standards.

The Group’s Discussion

The Group agreed with the analysis.

Overall, the Group’s discussion raised awareness of the potential implications of the amendments to IAS 12 for deferred taxes related to assets and liabilities arising from a single transaction. No further action was recommended to the AcSB.

Back to top

Subsidiary’s Accounting for a Spin-off Transaction

The Group considered the following fact pattern of a spin-off transaction in which shareholders of a parent entity receive shares of a newly created subsidiary that holds assets or businesses transferred from the parent entity. The Group discussed the subsidiary’s accounting for this transaction.

Fact Pattern

- An entity, ParentCo, decides to spin-off one of its non-core assets (e.g., a mineral property) to its shareholders. ParentCo’s shares are listed on a stock exchange and it has many shareholders. No shareholder or group of shareholders can exercise control over ParentCo. ParentoCo controlled the assets for several years prior to the transaction.

- To conduct the spin-off transaction, ParentCo creates a wholly owned subsidiary (“SpinCo”) and then concurrently:

- assigns the asset to that subsidiary in return for shares of SpinCo;

- distributes SpinCo’s shares to its shareholders; and

- applies to list SpinCo’s shares on a stock exchange.

The completion of the spin-off transaction was not contingent on the completion of the listing of SpinCo’s shares on a stock exchange.

- The entity transfers assets with a carrying value of $1 million to SpinCo in return for shares of SpinCo. The fair value of the assets transferred is $1.5 million.

- Since the asset is not controlled by the same party or parties before and after the spin-off transaction, this transaction is within the scope of IFRIC 17 Distributions of Non-cash Assets to Owners, for ParentCo. Therefore, ParentCo should record a dividend payable of $1.5 million in its financial statements.

Issue 1: Assuming the assets acquired do not meet the definition of a business, how should SpinCo measure the assets acquired from ParentCo and the shares issued?

View 1A – The assets acquired and equity issued should be measured at the asset’s fair value.

Proponents of this view think IFRS 2 Share-based Payment applies to this transaction because SpinCo acquired the assets through the issuance of its shares. IFRS 2 generally requires that the shares issued be measured at the fair value of the assets received. This is also consistent with the accounting for the transaction under IFRIC 17 where ParentCo records a dividend payable to its shareholders (i.e. SpinCo’s shares) at the fair value of the assets to be distributed.

Proponents of this view also acknowledge that the shares issued at fair value provides transparent and meaningful information to financial statement users.

View 1B – The assets acquired should be measured at ParentCo’s carrying value, and the equity issued measured at fair value or carrying value.

Proponents of this view think that paragraph 4 of IFRS 2 scopes out this spin-off transaction. As IFRS 2 does not apply, they note no other IFRS Accounting Standards provide specific guidance to assess whether to record the shares issued at their fair value or at the carrying amount of the assets in the financial statements of ParentCo.

Both the asset and the equity would be measured at ParentCo’s carrying value of $1 million. Therefore, SpinCo’s accounting is as follows:

| Dr. Assets |

$1 million |

| Cr. Common shares |

$1 million |

Alternatively, the common shares could be measured at fair value with a further adjustment to another component of equity. Therefore, SpinCo’s accounting is as follows:

| Dr. Assets |

$1 million |

| Dr. Equity reserve |

$0.5 million |

| Cr. Common shares |

$1.5 million |

View 1C – There is an accounting policy choice.

Since there is no specific guidance in IFRS Accounting Standards on this issue, SpinCo can establish an accounting policy and apply it consistently to all similar transactions.

The Group’s Discussion

Group members expressed diverse views on this issue.

Some Group members supported View 1A. They thought since the fact pattern stated that the asset was not controlled by the same party or parties before and after the spin-off transaction, the transaction was not between entities under common control. They also noted it was unclear how paragraph 4 of IFRS 2 would apply to this transaction and thus the transaction should be accounted for under IFRS 2.

Some other Group members supported View 1B. They thought the steps conducted in the spin-off transaction should be viewed in sequence as the ParentCo needs to first obtain the shares of SpinCo in step (a) before distributing them to its shareholders (steps (b) and (c)). They considered that step (a) to transfer the asset in return for SpinCo’s shares is a transaction between entities under common control. Therefore, they thought paragraph 4 of IFRS 2 would apply and that this transaction would be excluded from the scope of IFRS 2. They also thought the transaction lacks economic substance because SpinCo is a wholly-owned subsidiary of ParentCo and therefore the ultimate ownership of the property has not changed. As a result, the asset should continue to be measured at the carrying value in ParentCo’s accounts. A representative from the Canadian Securities Administrators (CSA) also supported this view when the steps involved in the spin-off transaction, as described in this fact pattern, are viewed in sequence.

A few Group members could not exclude either View 1A or 1B based on the rationale described above.

In terms of the measurement of common shares in View 1B, Group members observed that there is no specific guidance for bifurcating the elements within equity. Consequently, as long as the net equity amount is $1 million, Group members found both presentation options (the carrying amount or the fair value with an offset equity reserve) to be acceptable. A few Group members also noted that the laws and regulations in a specific jurisdiction could impact how equity should be measured and should be considered. That said, some Group members found that presenting the common shares at carrying amount to be more intuitive and more common in practice.

Issue 2: Assuming the assets acquired meet the definition of a business, how should SpinCo measure the assets acquired from ParentCo and the shares issued?

Analysis

SpinCo is an entity newly formed to issue equity instruments to effect a business combination. Therefore, SpinCo cannot be identified as the acquirer. Further, the acquired business cannot be identified as the acquirer in a reverse acquisition because SpinCo is not a business. Therefore, the transaction is outside the scope of IFRS 3 Business Combinations.

Only in limited circumstances would it be possible to identify SpinCo as the acquirer under IFRS 3. One such scenario would be if the transaction was contingent on completion of an initial public offering resulting in a change of control over SpinCo. In that case, applying the acquisition method would result in fair values being attributed to the assets acquired. In the fact pattern, since the completion of the spin-off transaction was not contingent on completing the listing of SpinCo’s shares on a stock exchange, SpinCo was not identified as the acquirer under IFRS 3.

The transfer of the business from ParentCo to SpinCo in return for shares of SpinCo does not have economic substance, therefore, when applying the IAS 8 hierarchy, SpinCo cannot elect to apply the IFRS 3 acquisition method. Accordingly, the financial statements of SpinCo should reflect the transaction as in substance a continuation of the business. Therefore, the assets acquired should be recorded at their carrying value.

The following three views consider how SpinCo should account for the equity issued:

View 2A – The shares issued should be valued at the fair value of ParentCo’s assets.

Proponents of this view would gross up the equity issued to the fair value of the assets, with a corresponding offset to another equity account. SpinCo’s accounting is as follows:

| Dr. Assets |

$1 million |

| Dr. Equity reserve |

$0.5 million |

| Cr. Common shares |

$1.5 million |

View 2B – The shares issued should be measured at ParentCo’s carrying value.

Both the assets and the equity should be measured at ParentCo’s carrying value of $1 million. SpinCo’s accounting is as follows:

| Dr. Assets |

$1 million |

| Cr. Common shares |

$1 million |

View 2C – There is an accounting policy choice.

Since there is no specific guidance in IFRS Accounting Standards on this issue, an entity can establish an accounting policy about whether to measure the shares issued at the carrying value of the assets or the fair value of the shares and apply it consistently to all similar transactions.

The Group’s Discussion

Group members observed that there is no specific guidance associated with bifurcating elements within equity. As such, most Group members thought an entity can establish an accounting policy about whether to measure the shares issued at the carrying value of the assets or the fair value of the shares (View 2C). That said, several Group members observed that View 2B is more commonly applied in practice. Furthermore, a few Group members thought as the transaction between ParentCo and SpinCo lacks economic substance, they found measuring the common shares at fair value to be counter-intuitive. Similar to Issue 1, these Group members thought the laws and regulations in a specific jurisdiction should be considered as they could impact how equity should be measured.

Issue 3: Assuming the assets acquired meet the definition of a business, for periods subsequent to the acquisition date, how should SpinCo present comparative information?

View 3A – SpinCo’s consolidated financial statements should include the results of the acquired business from the acquisition date only.

Proponents of this view think that financial statements should include the results of the business acquired from the date of acquisition only. Comparative information and the current period prior to the acquisition should not be restated.

For offering documents or other prospectus type disclosure (e.g. prospectuses, management information circulars, or offering memorandum), in addition to the presentation and disclosure requirements of IFRS, the applicable requirements of Canadian securities legislation may need to be considered. For example, since management plans to list SpinCo’s shares on an exchange following the transaction, investors will need to have a complete picture of the mineral property’s history (e.g. historical exploration expenditures incurred on the property).

In Canada, a prospectus should include information concerning the business conducted or to be conducted by the issuer that is sufficient to enable an investor to make an informed investment decision. This includes separate historical financial information of the predecessor entity or some other means of carve-out historical information, to convey what activity has occurred to develop the mineral property.

View 3B – Comparative information should be presented as though the entities had been combined throughout the periods presented

Proponents of this view note that since the transfer of the business from ParentCo does not have economic substance, the financial statements of SpinCo should reflect the transaction as a continuation of the business as it was presented in ParentCo’s financial statements throughout all the periods presented.

The Group’s Discussion

Some Group members noted that as indicated in the analysis for Issue 2, the spin-off transaction is outside the scope of IFRS 3. Furthermore, given the transfer of the business from ParentCo to SpinCo lacks economic substance, the financial statements of SpinCo should reflect the transaction as a continuation of the business with the assets acquired recorded at their carrying value. These Group members observed that in this scenario, it is common for Canadian entities to follow View 3B to present comparative information.

One Group member observed that the Ontario Securities Commission issued a Financial Reporting Bulletin in 2012 that strongly recommends presenting comparative information. Another Group member commented that presenting comparative information improves comparability and relevancy of financial information for investors.

Issue 4: Assuming the assets acquired do not meet the definition of a business, for periods subsequent to the acquisition date, how should SpinCo present comparative information?

Analysis

If the assets acquired do not meet the definition of a business and View 1A is applied in Issue 1, this results in a new basis of accounting for the assets acquired.

Consistent with the business acquisition scenario in Issue 3, the financial statements for periods subsequent to the acquisition date should include the results of the assets acquired from the date of acquisition only. Comparative information and the current period prior to the acquisition should not be restated.

SpinCo would also need to include additional historical financial information in an offering document filed for securities law purposes (e.g., historical financial information of the predecessor entity or some other means of carve-out historical information) to convey what activity has occurred to develop the mineral property.

The Group’s Discussion

One Group member agreed that if following IFRS 2, the entity creates a new basis of accounting for the assets acquired, and as such the comparative information should not be restated.

A representative of the CSA commented that even if the assets do not meet the definition of a business in IFRS Accounting Standards, the acquisition of these assets may constitute an acquisition of business under securities law. Therefore, in this situation, the securities law requirements set out in the prospectus rules would apply. Entities are encouraged to review the companion policy to the prospectus rules that was issued in 2022 for additional guidance.

Overall, the Group’s discussion raised awareness of the subsidiary’s accounting for a spin-off transaction. No further action was recommended to the AcSB.

Back to top

IFRS 9: Cash Received via Electronic Transfer as Settlement for a Financial Asset5

At its December 2021 meeting, the Group discussed a tentative agenda decision published by the IFRS® Interpretations Committee (the Interpretations Committee) related to the recognition of cash received via an electronic transfer system as settlement for a financial asset. At that meeting, the Group agreed with the Interpretations Committee’s technical analysis of the fact pattern included in the tentative agenda decision. The Group then discussed practical implications of implementing the tentative agenda decision if the Interpretations Committee finalizes it. For a summary of the Group’s discussion, see the Report on the Public Meeting on December 15, 2021.

At its June 2022 meeting, the Interpretations Committee reviewed comment letters on its tentative agenda decision, and ultimately voted to finalize the agenda decision, with some minor wording changes. The Interpretations Committee concluded that “the principles and requirements of IFRS Accounting Standards provide an adequate basis for an entity to determine when to derecognize a trade receivable and recognize cash received via an electronic transfer system as settlement for that receivable. Consequently, the Interpretations Committee decided not to add a standard-setting project to the work plan.”6

Paragraph 8.7 of the IFRS Foundation’s Due Process Handbook (Due Process Handbook) indicates that before an agenda decision is published, the IASB must vote on whether it objects to the agenda decision. This agenda decision is scheduled to be voted on by the IASB at its September 2022 meeting. In the IASB staff paper on this topic, the IASB staff summarized the Interpretations Committee’s previous discussions, and reported a summary of respondents’ comments on the potential outcomes of finalizing the agenda decision. The IASB staff recommended the IASB explore narrow-scope standard setting in response to the challenges raised by respondents to the tentative agenda decision. On balance, the IASB staff thought it is possible that the benefits of narrow-scope standard-setting could outweigh the costs.7 The Group first discussed the challenges raised by respondents to the agenda decision.

Issue 1: Challenges raised by respondents to the agenda decision

Analysis

The IASB staff paper summarized the following four themes from the comment letters to the tentative agenda decision:

- Disruption to long-standing accounting practices;

- Unintended consequences for other fact patterns;

- The agenda decision will be costly and complex to apply; and

- The agenda decision should not be finalized.

The Group discussed some of the challenges at its December 2021 meeting, including the implication of the agenda decision for the settlement of financial liabilities, and payment systems and settlement forms other than the one described in the submission to the Interpretations Committee.

The Group’s Discussion

The Group agreed with the analysis.

Some Group members pointed out that the agenda decision, if finalized, would not significantly impact most entities within the narrow fact pattern described in the submission. However, several Group members noted that the agenda decision might impact the accounting for many analogous fact patterns. Some of these fact patterns are accounted for using longstanding accounting practices, such as the derecognition of a trade payable upon the issuance of a cheque to a vendor. Some Group members questioned whether changing such longstanding accounting practices would result in information that is useful to financial statement users. The extent of analogous fact patterns, and the impact of the agenda decision on those fact patterns, were not analyzed by the Interpretations Committee as part of their agenda decision. As a result, some Group members indicated that it is unclear how entities might be required to apply this agenda decision to other fact patterns. A few Group members noted that this uncertainty might lead to inconsistent application of the requirements among entities, which may lead to other unintended consequences, including inconsistencies in the calculating certain debt covenants (e.g., net debt or working capital ratios).

One Group member thought that this agenda decision, if finalized, would have a pervasive impact across almost every entity if it is applied to all analogous fact patterns. This Group member noted that the work effort required for many entities to comply with the agenda decision would be significant. This work effort would be particularly significant for entities that operate in multiple jurisdictions since each jurisdiction might have different laws regarding legal settlement of financial assets and liabilities. Entities would therefore be required to undertake a detailed legal analysis in each jurisdiction where they operate, along with an analysis of the unique characteristics of their accounting and settlement systems.

One Group member highlighted some of the uncertainty regarding the potential application of this agenda decision to the derecognition of trade payables. Although the agenda decision does not directly discuss the derecognition of trade payables, this Group member noted that the principles in the agenda decision could be applied to trade payables by analogy. This Group member noted that there are theoretically three points in time when an entity might consider derecognizing a trade payable:

- when the payment is initiated;

- when the cash leaves the entity’s bank account; or

- when the counterparty receives the payment in their bank account.

They noted that the draft agenda decision implies that an entity should derecognize a trade payable when the counterparty receives the payment in their bank account. They noted that most entities do not normally contact their counterparties to confirm when they receive a payment, and that doing so would be impractical. They also questioned whether an entity would be required to recognize a receivable from their bank after the cash is removed from their account but before it is successfully delivered to the recipient/vendor. If this is the case, this Group member questioned whether the entity could then consider applying the offsetting guidance in paragraph 42 of IAS 32, Financial instruments: Presentation, to the offsetting payable and receivable balance on their balance sheet since these balances would be settled simultaneously.

One Group member suggested that the concerns stakeholders raised might be mitigated through narrow-scope standard setting. For example, the IASB could explore the possibility of including a settlement date/trade date accounting policy choice for payments in transit.

The Group then discussed the implications of the IASB staff’s recommendation to be considered by the IASB at its September 2022 meeting.

Issue 2: Implications of adopting the agenda decision if the IASB accepts the staff paper recommendation to explore narrow-scope standard-setting

Analysis

If the IASB accepts the staff recommendation to explore narrow-scope standard-setting at its September 2022 meeting, the final agenda decision will not be published. Until the IASB either objects to the Interpretations Committee’s agenda decision, does not object to the Interpretations Committee’s agenda decision or finalizes any standard-setting, there remains a question whether entities should apply the guidance in the unpublished agenda decision in the meantime.

View 2A – As the steps to finalize the agenda decision have not been completed and further standard-setting is being considered, there is no requirement for entities to adopt the unpublished agenda decision and change accounting practices where inconsistent with the analysis and conclusions presented by the Interpretations Committee.

Proponents of this view point out that if the IASB accepts the IASB staff’s recommendation in the agenda paper to explore narrow-scope standard setting, the IASB will not be asked whether they object to the Interpretations Committee’s agenda decision and the original agenda decision will not be finalized or published. Without this final step in the due process, a finalized agenda decision will not exist. Thus, it is unclear whether the additional insights on the application of existing standards must be considered by entities.

In addition, proponents of this view note that the completion of a standard setting project (if any) might confirm that an entity’s current accounting practices are permitted. In that case, an entity that changes accounting practice to adopt the guidance in the agenda decision, might then be required to revert to their original accounting treatment once the IASB completes its standard setting activities. Therefore, requiring entities to change their current accounting practices to reflect adoption of the unpublished agenda decision would introduce incremental costs that ultimately may be redundant.

View 2B – As the steps to finalize the agenda decision have not been completed and further standard-setting is being considered, there is no requirement for entities to adopt the unpublished agenda decision. However, entities could consider the unpublished agenda decision as providing additional insights, and change their accounting practices to provide more useful information to users.

Proponents of this view refer to paragraph 8.6 of the Due Process Handbook which states that “the explanatory material may provide additional insights that might change an entity’s understanding of the principles and requirements in IFRS Accounting Standards. Because of this, an entity might determine that it needs to change an accounting policy as a result of an agenda decision.” Therefore, an entity could consider the unpublished agenda decision while assessing its existing accounting practices. If the entity’s existing accounting practice is inconsistent with the analysis and conclusions presented in the unpublished agenda decision, the entity could change those accounting practices.

View 2C – Given the Interpretations Committee has concluded that existing IFRS Accounting Standards provide an adequate basis for determining the accounting treatment in the submitted fact pattern, entities should adopt the agenda decision and change accounting practices where inconsistent with the analysis and conclusions the Interpretations Committee presented.

Proponents of this view point out that agenda decisions do not add or change requirements in IFRS Accounting Standards – they simply explain how the applicable principles and requirements of the standards apply to a specific transaction or fact pattern. Almost all respondents to the tentative agenda decision agreed (or did not disagree) with the Interpretations Committee’s technical analysis and conclusions, and the Interpretations Committee ultimately voted to finalize the tentative agenda decision. Therefore, the unpublished agenda decision should be adopted as part of an entity’s understanding of the principles and requirements in existing standards.

Proponents of this view think the timeframe for entities to consider the need to change their accounting practices, and for implementing such changes should follow the same guidance in the Due Process Handbook as for published agenda decisions. Therefore, entities are entitled to “sufficient time” to implement an Interpretations Committee’s agenda decision. Entities should refer to the IASB article, “Agenda decisions – time is of the essence” and the Due Process Handbook, Sections 8.2-8.7 for guidance on the timely implementation of agenda decisions.

The Group’s Discussion

Most Group members agreed with View 2A. They noted that the Due Process Handbook was recently amended to promote consistent application of IFRS Accounting Standards, and that circumventing this process could result in less comparable information among entities. Furthermore, they noted that the IASB staff recommends the IASB explore a standard-setting solution to address stakeholders’ concerns with the cost of applying the guidance to all analogous fact patterns and the decision-usefulness of the resulting information. Depending on the outcome of any potential standard-setting project, entities may ultimately be permitted to continue their current accounting practices.

Some Group members indicated that they agree with the technical analysis in the draft agenda decision as it applies to the narrow fact pattern in the submission. They questioned whether it is reasonable for entities to defer the application of the draft agenda decision when it provides a valid interpretation of existing standards. They also think that entities could consider applying the guidance to similar fact patterns to the one in the submission (i.e., an electronic transfer of cash for settlement of a trade receivable).

One Group member noted that entities should evaluate the changes they would need to make to their existing processes if the agenda decision is finalized. This could include an analysis of the transactions that would be in scope, and the system changes or manual processes that would need to be implemented to apply the guidance. This Group member indicated that the changes might not be as significant as anticipated for some entities.