Thank you to all who provided feedback on the AASB’s Exposure Draft, “Proposed Canadian Standard on Sustainability Assurance (CSSA) 5000, General Requirements for Sustainability Assurance Engagements."

The Auditing and Assurance Standards Board (AASB) is now considering the feedback you provided – including what possible revisions might be required for Canada’s adoption of this international standard.

What we heard

Based on what we heard, feedback gathered in Canada is generally consistent with the main feedback themes heard in response to the international standard’s consultation. These themes include:

- Relevant ethical requirements: More guidance requested on the concept of "at least as demanding" with respect to relevant ethical requirements and quality management.

- Relationship between proposed ISSA 5000, General Requirements for Sustainability Assurance Engagements and ISAE 3410, Assurance Engagements on Greenhouse Gas Statements: Additional clarity is needed about when ISAE 3410 applies.

- Entity’s “materiality process”: This process needs further consideration, such as guidance on the practitioner’s evaluation or assessment of the process – with a focus on completeness.

- Practitioner’s materiality: Materiality needs to be addressed in greater detail, including application material for qualitative disclosures.

- Estimates and forward-looking information: More guidance requested on obtaining evidence for estimates, forward-looking information, and information from the value chain.

- Group sustainability assurance engagements: Additional requirements and guidance requested for group sustainability assurance engagements.

- Implementation guidance: The need for first-time implementation guidance was identified.

Areas where feedback gathered in Canada was contrary to feedback heard during the international consultation process include:

- Greenwashing: Canadian respondents noted that the proposed standard sufficiently addresses the concept of greenwashing and other types of washing (e.g., social washing), by focusing on the susceptibility of the sustainability information to material misstatement, whether due to fraud or error; and

- External expert: Using the work of a practitioner’s external expert or another practitioner and the related requirements are clear and capable of consistent implementation.

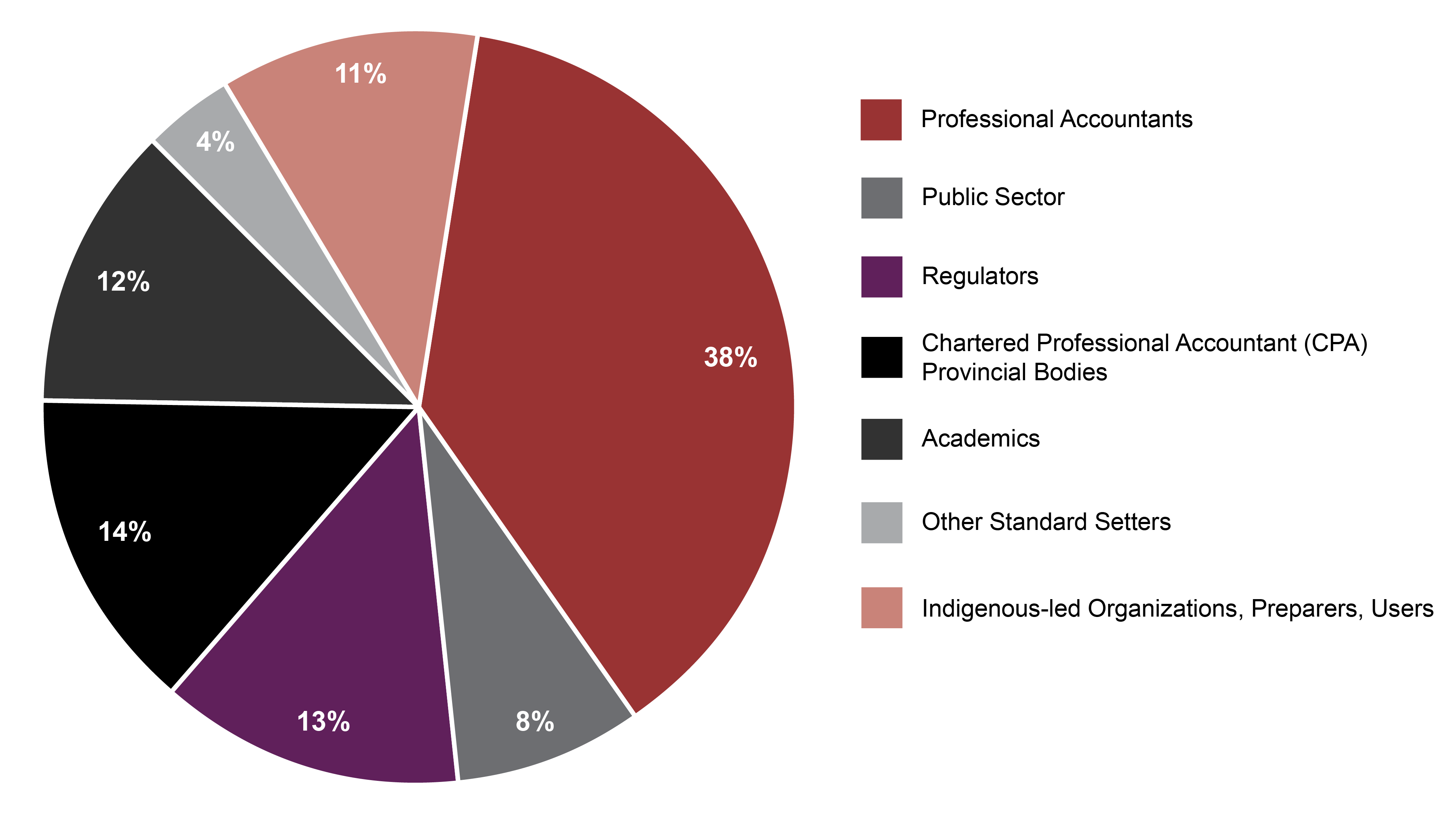

Who we heard from

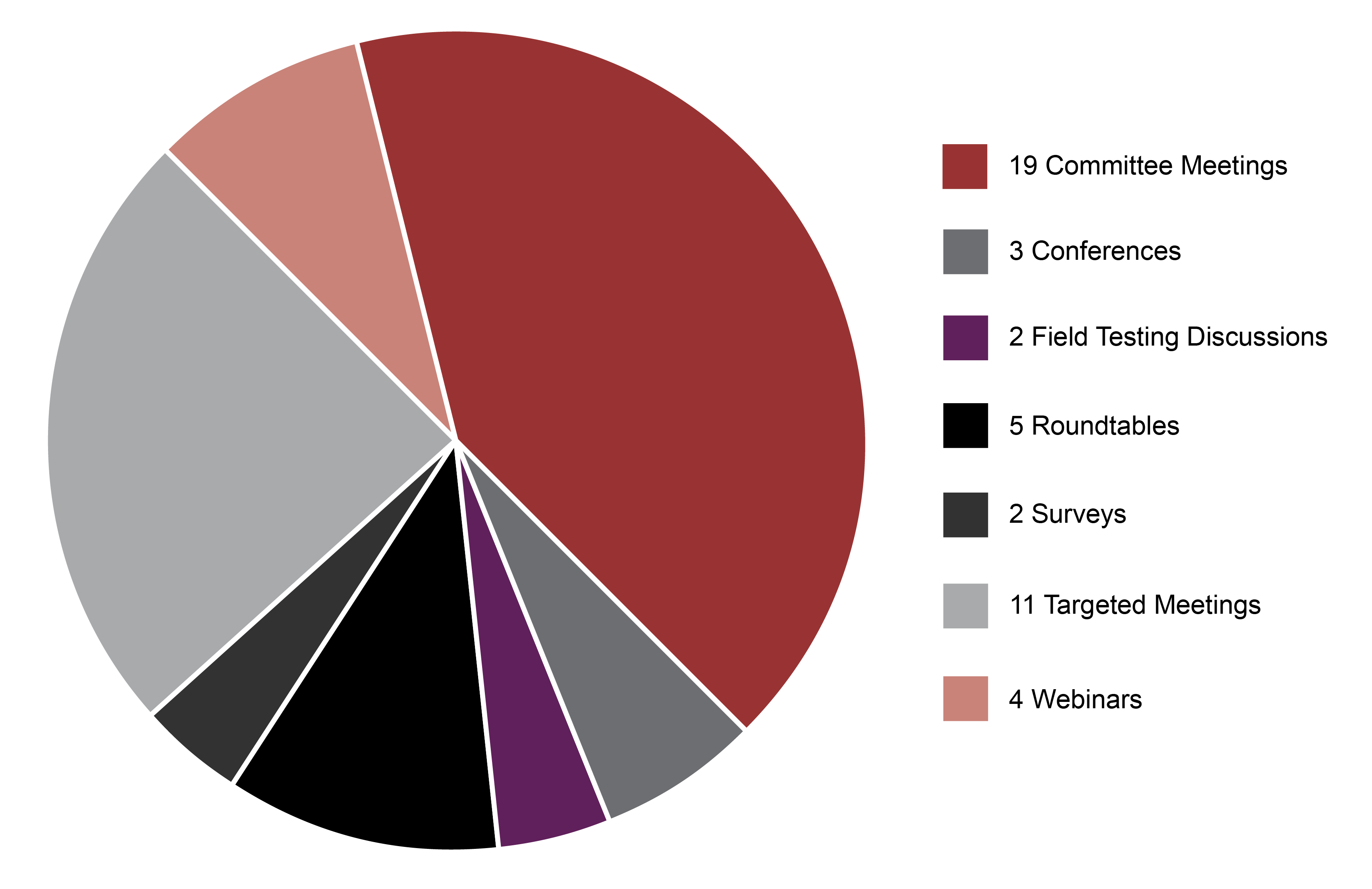

How we gathered your feedback

What’s next

Over the next few months, the AASB will be working to ensure Canadian feedback is considered by the International Auditing & Assurance Standards Board (IAASB) as the final standard is developed. The anticipated approval date for the final CSSA 5000 is December 2024.