The Accounting Standards Board (AcSB) considered an issue that stakeholders raised about using the funding valuation in the measurement of the defined benefit obligation in relation to Ontario’s Provision for Adverse Deviations (PfAD issue). The AcSB was concerned about potential diversity in practice that could arise. The AcSB decided not to undertake any standard-setting action on the PfAD issue, but rather communicate its intent. The AcSB wrote a letter to the Canadian Institute of Actuaries to communicate its intent. The key points from this letter have been summarized below, along with additional background information.

Background

Regulation

In April 2018, Ontario’s pension regulator introduced a new reserve — a PfAD — in the going concern funding valuation for defined benefit pension plans.

PfAD issue

The AcSB considered whether the PfAD should or should not be included in the measurement of the defined benefit obligation when an entity elects to use a funding valuation in accordance with Section 3462, Employee Future Benefits, in Part II of the CPA Canada Handbook – Accounting.

Application

The AcSB is concerned about potential diversity in practice that could arise from stakeholders applying Section 3462 either:

- directly as a private enterprise that applies Part II of the Handbook;

- via Section 3463, Reporting Employee Future Benefits by Not-for-Profit Organizations, in Part III of the Handbook; or

- via Section 4600, Pension Plans, in Part IV of the Handbook.

Key points on PfAD issue

The use of a funding valuation in Section 3462 was an accommodation to eliminate the additional costs of preparing a separate accounting valuation. A funding valuation is not management’s best estimate of the defined benefit obligation; an accounting valuation is management’s best estimate.

Section 3462 states that a funding valuation is prepared in accordance with legislative, regulatory, or contractual requirements. The funding valuation is the amount at which the legislation, regulation or contract requires funding. When such requirements stipulate separate calculations of various components of the funding requirement, it is the aggregate of those components that make up the funding valuation to be reflected in the financial statements. Accordingly, the measurement of the defined benefit obligation in the financial statements reflects the aggregate of the components of the funding valuation. For example, the PfAD is one of those components of the funding valuation that would be included in the measurement of the defined benefit obligation.

Stabilization Provision issue

In addition to the PfAD introduced by Ontario’s pension regulator, Quebec’s pension regulator established a new regulation in 2016 for private sector plans in that province — the Stabilization Provision. The AcSB has been considering an application issue regarding this Stabilization Provision and Section 3462 for which diversity has been arising in practice. Read about the AcSB’s project to consider this issue in developing an exposure draft, including summaries of the AcSB’s discussions of this topic to date.

Defined benefit plans without a funding valuation requirement issue

The AcSB has also considered an issue that relates to both provisions and Section 3462 in relation to defined benefit plans without a funding valuation requirement. Diversity has been arising in practice as to whether the PfAD and the Stabilization Provision should be included in the measurement of the defined benefit obligation when an enterprise elects to use a funding valuation for defined benefit plans for which there is no legislative, regulatory or contractual requirements to prepare a funding valuation. An example of such a plan is an unfunded defined benefit supplemental executive retirement plan offering pension benefits.

In particular, the AcSB considered paragraph 3462.029C, which states:

“For other defined benefit plans, there is no legislative, regulatory or contractual requirement to prepare an actuarial valuation for funding purposes. For these plans, the entity shall make an accounting policy choice, on a plan-by-plan basis, to measure the defined benefit obligation as of the balance sheet date using:

(a) an accounting valuation; or

(b) a funding valuation, provided that the entity also has at least one defined benefit plan for which a funding valuation is required to be prepared in order to comply with legislative, regulatory or contractual requirements and for which the defined benefit obligation has been measured using a funding valuation.

For a defined benefit plan for which there is no legislative, regulatory or contractual requirement to prepare an actuarial valuation for funding purposes, the funding valuation is an actuarial valuation prepared on a basis consistent with that used for those plans for which a funding valuation is required to be prepared in order to comply with legislative, regulatory or contractual requirements.” [emphasis added]

Specifically, the AcSB discussed the meaning of “on a basis consistent with”. The AcSB agreed that its intent was that “on a basis consistent with” is equivalent to “the same”. Accordingly, the PfAD and Stabilization Provision should be included in the measurement of the defined benefit obligation for these defined benefit plans.

The AcSB understands that some enterprises, consistent with their approach for funded defined benefit plans, did not include the relevant provision in the measurement of the defined benefit obligation for unfunded defined benefit plans. Accordingly, the AcSB plans to consider including this issue, along with any transitional provisions, in developing the aforementioned exposure draft.

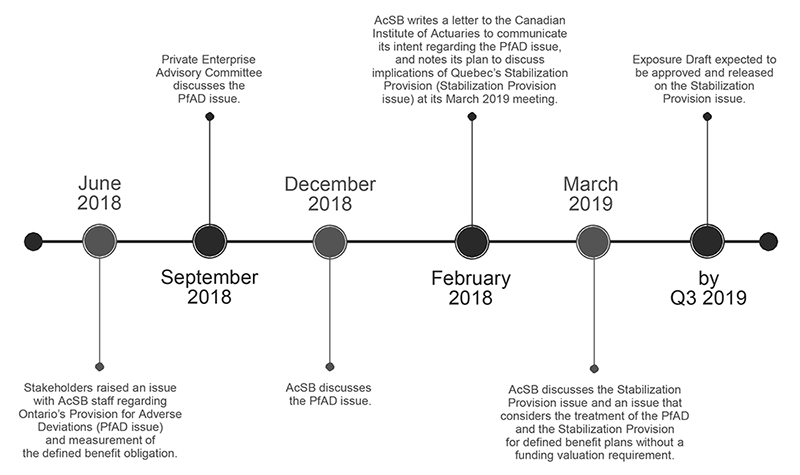

Timeline

Below is a timeline of the AcSB’s activities on the PfAD issue as well as the related issues on the Stabilization Provision and both provisions regarding defined benefit plans without a funding valuation requirement.