How we serve the public interest

We establish high-quality accounting standards that promote confidence in the information reported by Canadian private sector entities. When developing these robust standards, we consider changes in the economy, as well as the costs and benefits to both preparers and financial statement users. We remain accountable to interested and affected parties by responding to their needs in a timely manner and facilitating their participation and input into the development of the standards that affect them.

We contribute to global best practices in accounting standard setting for every major reporting entity category in Canada’s private sector: publicly accountable enterprises, private enterprises, not-for-profit organizations (NFPOs), and pension plans.

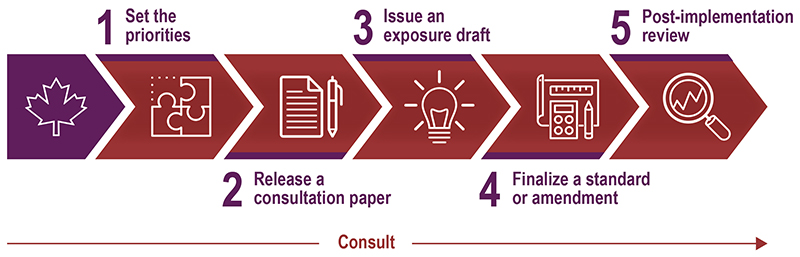

We follow a due process based on three principles: transparency, consultation, and accountability. These principles permeate the due process procedures we follow when determining the content of the CPA Canada Handbook – Accounting (the “Handbook”) applied by all reporting entities in Canada.

Domestic Accounting Standards Due Process

IFRS® Accounting Standards Due Process

Back to top

Overview

Our strategy

Our 2022-2027 Strategic Plan focuses on enhancing the relevance of financial and non-financial information reported to meet the evolving information needs of Canadian interested and affected parties. Our core strategies will best support achieving this mandate.

How we will achieve our strategy

This Annual Plan is based on the vision, mission, and strategic objectives set out in our 2022-2027 Strategic Plan. It outlines the activities we plan to undertake in the third year of our five-year Strategic Plan to achieve our major goals.

In delivering high-quality accounting standards, we recognize that guidance is needed in today’s continually evolving environment. In the 2023-2024 fiscal year, we developed a framework to respond to interested and affected parties in their need for additional guidance when applying Parts II and III of the Handbook. Our focus in 2024-2025 will be on the implementation of this framework.

We will maintain our focus on enhancing the relevance of accounting standards. In response to the feedback received on Consultation Paper I, “Exploring Scalability in Canada” issued in 2023-2024, we will conduct a detailed review of Accounting Standards for Private Enterprises (ASPE) to determine how the standards can best meet the needs of interested and affected parties. As part of our detailed review of ASPE, we will also consider the feedback we heard on our Domestic Work Plan Survey issued in the 2023-2024 fiscal year.

For entities that apply IFRS® Accounting Standards, we will also continue to be responsive to emerging issues in the Canadian environment by advancing our research in areas such as intangible assets, carbon credits, and cash flow reporting. We will use this research to help inform future international discussions on these topics.

Remaining focused on the interconnectivity between financial reporting and sustainability will be a key consideration in the coming year. In the 2023-2024 fiscal year, the International Sustainability Standards Board (ISSB) issued its first sustainability standards and performed consultations on its future agenda priorities. Additionally, the Canadian Sustainability Standards Board (CSSB) was established and became fully operational. We will work together with the CSSB and the International Accounting Standards Board (IASB) to ensure that Canadian perspectives continue to be considered internationally.

We now host more in-person events that enable impactful discussions on key issues facing the Accounting Standards Board (AcSB). We look forward to continuing to use these events to better connect with interested and affected parties and allow them to engage with us on issues that matter to them. At the same time, we will continue to be mindful of our carbon footprint.

Back to top

Strategies for Each Part of the Handbook

Part I: Support the application of IFRS® Accounting Standards in Canada

Our objectives

We believe that supporting implementation starts at the beginning of a standard’s development. As a result, we will continue working to influence the IASB throughout its standard-setting process, leveraging our reputation to make advancements. We will also work to provide a direct line of contact to the IASB for interested and affected parties whenever possible.

We support interested and affected parties with implementation through targeted activities:

- Influence: We will perform the appropriate level of consultation on documents for comment issued by the IASB to the extent they are relevant to Canadian interested and affected parties.

- Monitor: We will closely monitor for application issues related to emerging issues and newly issued amendments. Our IFRS® Accounting Standards Discussion Group is an important part of all these activities. We will work with this Group to identify implementation issues affecting Canadians through open communication and robust agendas.

- Committee support: We will maintain an open dialogue with our advisory committees as needed, including the Academic Advisory Committee and User Advisory Committee, to ensure Canadian-specific issues are considered. Through our Crypto-asset Working Group, we will continue to monitor the accounting for and disclosure of crypto-asset activities.

Similar financial reporting outcomes under IFRS Accounting Standards and U.S. generally accepted accounting principles (GAAP) are highly important for interested and affected parties. We will continue to work toward narrowing new, unnecessary differences in financial reporting outcomes under IFRS Accounting Standards and U.S. GAAP by regularly engaging with the IASB and U.S. Financial Accounting Standards Board. We will also leverage our relationships with other national standard setters.

Part II: Continue to establish appropriate accounting standards for private enterprises

Our objectives

Our main priorities for 2024-2025 continue to be improving financial reporting for private enterprises and addressing areas that are causing them difficulties. Our guidance framework, developed in the 2023-2024 fiscal year, will help us to identify needs for additional guidance when applying domestic accounting standards and determine the best way to respond to interested and affected parties.

In line with our 2022-2027 Strategic Plan, we will focus on enhancing the relevance of accounting standards in Part II of the Handbook. In response to the feedback on Consultation Paper I, “Exploring Scalability in Canada,” we will conduct a detailed review of ASPE to identify specific challenges entities are facing in each standard and potential solutions.

We will also advance our planned activities on priority projects, including a project to address the challenges related to the subsequent measurement of goodwill and recognition of intangible assets acquired in a business combination. Additionally, we will consider feedback received from our exposure draft related to the accounting for life insurance contracts with cash surrender value and issue the Accounting Guideline. We will also issue amendments to the revenue standard to defer indefinitely the effective date of guidance relating to upfront non-refundable fees or payments and introduce a new related disclosure requirement. Finally, we will review the financial statement concepts in the Handbook. We are continually listening to interested and affected parties to ensure we are aware of new and emerging issues facing Canadian private enterprises.

We are also committed to assessing the effect of new standards or major amendments to ensure consistent application. As a result, we plan on preparing for a post-implementation review of the amendments for retractable or mandatorily redeemable shares issued in a tax-planning arrangement and will consult with interested and affected parties when timing is appropriate.

Our Private Enterprise Advisory Committee, Small Practitioners Working Group, and Agriculture Advisory Group will continue to support high-quality and timely implementation and solutions by identifying and assessing application issues and providing recommendations to address them.

Part III: Continue to establish appropriate accounting standards for NFPOs

Our objectives

We are dedicated to ensuring NFPO standards reflect the current environment and supporting interested and affected parties in applying the standards. Advancing our Contributions project is a key priority in 2024-2025. We received extensive feedback on our Exposure Draft, “Contributions – Revenue Recognition and Related Matters,” which was issued in the 2023-2024 fiscal year. As we head into 2024-2025, we will issue a Feedback Statement summarizing the views expressed on the Exposure Draft and providing an overview of the proposed next steps. We will respond to the feedback and continue to engage with the NFPO sector to ensure that the contributions standard meets the needs of interested and affected parties. Additionally, we will continue to engage with the NFPO sector as we start developing proposals on the reporting of controlled and related entities. Where appropriate, we will align work on Part II projects with Part III.

We will also respond to the needs of interested and affected parties through our guidance framework and provide implementation guidance for the sector through tools such as webinars and In Briefs.

We will look to our Not-for-Profit Advisory Committee for support to address feedback on our Exposure Draft, “Contributions – Revenue Recognition and Related Matters.” The Committee will also continue to support high-quality and timely implementation and application solutions by identifying and assessing application issues and providing recommendations to address them.

Part IV: Enhance the relevance of accounting by pension plans

Our objectives

We will continue to ensure that Part IV standards meet the needs of this sector.

To do this, we will work with our Pension Plan Advisory Committee to consider proposals to improve the presentation and disclosure requirements related to investments held by pension plans. Our aim is to issue an exposure draft of these proposals during the 2024-2025 fiscal year.

Our expert Committee will also continue to support us in identifying future areas of focus to enhance the relevance of accounting by pension plans.

Preface to the Handbook

Our objectives

We will advance research on our project for improving the Preface to the Handbook to ensure it remains fit for purpose for reporting entities and the users of their financial statements.

We recognize that practitioners servicing smaller businesses have important insight to share on this topic, so we will continue to consult our Small Practitioners Working Group to advance this important strategic work.

Back to top

Support Improving the Quality of Reporting Beyond the Traditional Financial Statements

Our objectives

We continue to see rapid change in the reporting needs of Canadian entities. Additionally, capital providers, investors, and interested and affected parties are demanding more transparency and decision-useful information beyond what is currently available in the traditional financial statements. In line with our vision, we are focused on identifying how best to support Canadian needs – inside and outside the traditional financial statements.

Our 2022-2027 Strategic Plan identifies strategies to do just that – helping financial statement users make well-informed, economic decisions and allowing financial statement preparers to explain their results in a cost-effective way. This includes continuing with our core mandate of serving the public interest through the development of accounting standards and other related reporting guidance.

In the 2023-2024 fiscal year, the ISSB issued its first sustainability standards, IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures, which will form a global baseline for the capital markets. The ISSB also consulted on its future agenda priorities. We will continue to participate in this global dialogue by working with the CSSB and other national standard setters to influence international discussions on the connectivity between financial and sustainability reporting.

Domestically, we will work with the newly operational CSSB and various regulators to identify opportunities and support the bringing together of financial and non-financial information relied on by financial statement users. Doing so will provide added insight to interested and affected parties in Canada with respect to a reporting entity’s financial performance.

Back to top

Grow the AcSB’s International Influence

Our objectives

One of our proudest achievements is the strong international reputation we have cultivated for Canadian standard setting. This could not have been achieved without the support of interested and affected parties in Canada.

We will continue to advance our effort in 2024-2025 and remain firmly seated at the international table when issues important to Canadians are discussed to ensure that the Canadian perspective is heard and considered.

We also plan to use the traction we have gained to grow our international influence for private enterprises, NFPOs, and pension plans. We will work to advance global standard setting by providing thought leadership and global best practices for all major reporting entity categories in Canada’s private sector.

To do this, we will continue to:

- maintain and grow strong strategic collaborations with standard setters across the world to amplify Canadian views on IFRS Accounting Standards, and discuss issues faced by private enterprises, NFPOs, and pension plans in Canada;

- significantly contribute at international meetings, such as the Accounting Standards Advisory Forum, World Standard Setters, International Forum of Accounting Standard Setters, and National Standard Setters Sustainability Forum, by sharing Canadian perspectives and practices on relevant issues; and

- support any Canadian(s) appointed to the IASB and other Canadians appointed to international committees, as well as recommend Canadians for appointments when opportunities arise.

Back to top

Monitor for Success

Due process

Our due process is based on three principles: transparency, consultation, and accountability. We are committed to following our due process in each decision we make and will consider other factors when applying due process to address extenuating circumstances. We will continue to look for ways to promote transparency in what we do. We aim to be even more accessible to interested and affected parties and expand the reach of our consultation activities. This is essential to our work.

Our overarching goals for governance also mean ensuring interested and affected parties can hold us accountable and understand the decisions we make. To support this, we will be clear, timely, and concise when sharing information.

Communications

The quality of everything we do is directly related to ensuring the lines of communication are open to interested and affected parties.

Our annual plan continues our focus on communication activities and aims to raise the level of awareness and engagement in our processes and activities. We will also consider additional outreach necessary to existing groups of interested and affected parties, as well as newly identified ones, as necessary.

Our risks

To make sure we achieve goals set in our annual and strategic plans, we monitor our progress, and identify and manage our risks effectively. This risk management process includes identifying mitigating controls and monitoring developments in the business environment. This helps ensure we know when to change our standard-setting approach.

Many of the key risks that we manage are operational in nature. We recognize the increased demand from interested and affected parties for guidance in applying domestic accounting standards, and addressing these demands that will impact our operations. Additionally, remaining relevant to interested and affected parties is a key priority to managing our strategic and reputational risks. As such, we are committed to staying nimble and re-evaluating priorities as needed. This includes trying new and innovative ways to progress projects and effectively engage with interested and affected parties.

Deliverables and timelines

Our project plan is based on best estimates of current staffing levels, Board-approved projects for domestic standards, and the latest information on the IASB’s work plan. We are ready to change our plans to ensure interested and affected parties are well served. We will communicate any changes and the reasons for them in a clear and timely manner.

Stay up to date on our current projects and activities:

Also see the IASB's work plan for additional information on IFRS Accounting Standards projects and the AcSB’s decision summaries that follow every meeting, which outline the work we do on domestic accounting standards and IFRS Accounting Standards.

For an overview of our past achievements, read our Annual Report.

Back to top